We use cookies to provide you with the best possible online experience. Read our cookie policy.

Media Release

02 June 2026

Middle East tensions interrupt business confidence recovery

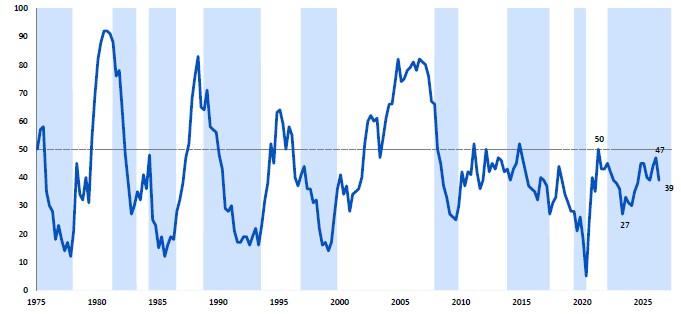

The RMB/BER Business Confidence Index (BCI) fell by 8 points to 39 in the second quarter of 2026, reversing the gains recorded over the previous two quarters and leaving the index just below its long-term average of 40. While the recovery in business sentiment has lost momentum, importantly, confidence remains well above the recent low of 27 reached in 2023Q2.

Figure1: RMB/BER Business Confidence Index (BCI)

% satisfactory

Source: BER, SARB (Shaded areas represent economic downswings)

The survey took place from 14 to 25 May 2026. During this period, the operating environment for firms deteriorated meaningfully from the first-quarter survey (conducted before the US/Iran war) as tensions in the Middle East escalated, driving oil and fuel prices higher. This also contributed to a marked shift in the domestic interest-rate outlook towards hikes. Whereas markets had previously expected further monetary policy easing, including around three 25 basis-point cuts, attention has since shifted to the possibility of between two and four rate hikes of 25 basis points each. Indeed, the policy rate was raised by 25 basis points after the survey period.

The decline in confidence is therefore not unexpected.

This change in the macroeconomic backdrop weighed on sentiment across most sectors. Four of the five sectors that make up the headline index recorded lower confidence in the second quarter. The largest decline was among new vehicle dealers, where confidence fell by 18 points to 49, followed by wholesalers, down 10 points to 40. Retail confidence declined by 5 points to 31, while building contractor confidence fell by 4 points to 46. Manufacturing was the only sector to record an improvement, albeit marginally, rising by 1 point to 31.

Details

The deterioration in confidence was broad-based, but not uniform. The sharpest pullback came from sectors most exposed to shifts in household spending, financing conditions and fuel costs.

Table: Business confidence per sector

|

Indicator |

LT avg. |

24Q2 |

24Q3 |

24Q4 |

25Q1 |

25Q2 |

25Q3 |

25Q4 |

26Q1 |

26Q2 |

change |

|

RMB/BER Business Confidence |

41 |

35 |

38 |

45 |

45 |

40 |

39 |

44 |

47 |

39 |

-8 |

|

New vehicle dealers |

39 |

10 |

27 |

23 |

52 |

42 |

54 |

58 |

67 |

49 |

-18 |

|

Retailers |

40 |

39 |

45 |

54 |

50 |

42 |

32 |

43 |

36 |

31 |

1 |

|

Wholesalers |

45 |

53 |

51 |

60 |

42 |

50 |

38 |

42 |

50 |

40 |

-10 |

|

Building contractors |

40 |

47 |

41 |

51 |

45 |

35 |

46 |

39 |

50 |

46 |

-4 |

|

Manufacturers |

34 |

28 |

28 |

36 |

34 |

33 |

23 |

39 |

30 |

31 |

1 |

New vehicle dealers remained the most confident sector despite the sharp decline in sentiment from the elevated level reached in the first quarter. The decline was accompanied by weaker sales volumes, suggesting that the earlier rapid momentum in vehicle demand has started to fade.

Wholesaler confidence declined materially, falling to 40 in the second quarter. Business conditions deteriorated, though they remained slightly better than they were this time last year. Consumer goods sales volumes declined sharply.

In line with underperforming consumer-facing wholesalers, retailers remained subdued, with confidence falling further to 31 after a decline to 36 last quarter. Retail sales volumes weakened sharply, particularly in semi-durable and durable goods, suggesting a more cautious consumer cutting back on discretionary spending.

Building contractor confidence eased to 46, following the strong improvement recorded in the first quarter. While the decline was relatively contained, activity weakened, with both residential and non-residential building activity under renewed pressure

Manufacturing confidence was the exception, edging up to 31. However, the level remains low and consistent with ongoing demand weakness. Domestic sales were unchanged at a weak level, although some export-related indicators improved. A surge in production costs has left the sector facing a challenging operating environment.

Provincially, the deterioration was concentrated in Gauteng and KwaZulu-Natal with declines of 15 points to 26 and 17 points to 40, respectively. By contrast, confidence in the Western Cape increased by 5 points to 55, making it the only major province to record an improvement.

Bottom line

According to Isaah Mhlanga, Chief Economist at RMB, The decline in business confidence during the second quarter is disappointing, particularly after the encouraging improvement re"corded over the preceding two quarters. However, the setback is not unexpected given the sudden deterioration in the global environment, even though there was no material weakening in South Africa's domestic fundamentals." Mhlanga adds that "the sharp escalation of tensions in the Middle East pushed oil prices higher, lifted local fuel costs and significantly altered interest-rate expectations. Businesses have had to adjust quickly to a less supportive outlook, which weighed on sentiment across most sectors. While firms continue to grapple with familiar domestic challenges, there is little evidence that these issues deteriorated further. Instead, many respondents indicated that uncertainty had increased and that clients had become more cautious about spending and investment decisions".

Importantly, confidence remains broadly in line with its long-term average and above the lows recorded in recent years. "While the external shock has interrupted the recovery in sentiment, it has not necessarily derailed it," says Mhlanga. "Much will depend on whether geopolitical tensions ease and whether domestic reform momentum can continue to support growth and investment."

The second-quarter survey suggests that businesses have become more cautious rather than outright pessimistic. Firms appear to be reassessing the outlook in response to a more uncertain global environment and the prospect of higher inflation and interest rates. A renewed improvement in confidence will depend on some easing in geopolitical tensions, a stabilisation in oil and fuel prices, and greater certainty about the interest-rate path. Continued progress on structural reforms, alongside improvements in logistics, infrastructure and local government performance, will be critical in ensuring that the current setback proves temporary rather than persistent.

Ends

Enquiries

Isaah Mhlanga

Chief Economist

Tel: 073 736 5357 / 011 282 1460

Isaah.Mhlanga@rmb.co.za